(L'argent magique des banques centrales lorsqu'on y a goûté, difficile de s'en passer, c'est tellement facile. Personnellement de l'argent magique, j'en ai pas vu un kopeck passé, sans doute il sert à nourrir le monde des bisounours des très riches. note de rené)

"The Straw That breaks The Market's Back": The Fed Must Do $3.9 Trillion In QT To Control Inflation... Which It Can't Possibly Do

Starting with first principles, there is one thing that almost all traders can agree on and it is that, sooner or later, the Fed tightening cycle will spark another financial crisis and market crash, something which we reminded readers in early 2022:

But while there is little disagreement on what the Fed's endgame is, the big question is how we get there and what exactly will lead to the overtightening that crashes the economy, sparks a policy panic and bring another Fed overreaction in the opposite direction.

For much of the past 6 months, Wall Street was confident that it would be the Fed's rate hikes which started in March from 0.0%, and have since crept up to 2.25-2.50%, and are expected to rise another 1.00%-1.25% before the Fed eases back on the breaks.

Incidentally, one of the reasons so many Wall Street professionals expected the Fed to pivot dovishly sooner rather than later, is that few expected the Fed would so aggressively seek to trigger then next recession, and to keep hiking until something did break. In fact, back in April SocGen quant Solomon Tadesse - who made waves on Wall Street trading desks four years ago, when he went against the consensus view, and in 2018 pinpointed the peak in Fed Funds at a lowly 2½% which turned out to be spot on - calculated that the Fed Funds rate won't be able to climb above 1.0% before the Fed overtightens into restrictive territory, i.e., will have to ease (the explanation for his thinking is here).

Of course, 4 months later and 1.5% above the proposed 1.0% "redline", Solomon's math was clearly wrong. But was he wrong or did the SocGen quant merely underestimate the far greater weight that the Fed's balance sheet, or QE (and thus QT) has on overall easing (and tightening) of financial conditions?

That is the topic Tadesse and his SocGen quant peers discuss in their latest Practical Quant Investor note, titled "Might QT be the straw that breaks the market's back", in which they note that in recent weeks, financial markets and monetary policy pronouncements seem too focused on the policy rate to deal with inflation containment. However, extending on what we said above, the SocGen quants note that "what has been unique in post-GFC monetary policy was the reliance on QE to induce the needed easing." As they also note, in recent years it was not policy rate hikes – which were on an orderly course – that laid low financial conditions, leading to a surprise pivot in monetary policy in December of 2018, but rather the quietly accelerating QT. By the same token, Tadesse warns "it could be a ramp-up in QT, this time on a larger scale to erode a much larger balance sheet, that could surprise markets." This is a prudent warning because three months after QT started at a pace of $47.5BN per month from June through August, starting Sept, the Fed will double the pace of Quantitative Tightening to $95Billion, draining twice as much liquidity from the market.

Before we delve deeper into the SocGen quant's analysis, let's first back up, and briefly discuss what happened in the post-June market meltup which as Tadasse puts it, until last week's hiccup, "was a byproduct global markets had recently been on a bullish ascent, buoyed by hopes of an easing in inflation and thus a Fed pivot. Yet, central bank policy pronouncements and policymakers have been quick to warn that this expectation is premature." Therefore, investors - SocGen summarizes - "face a historic dilemma: a choice between the two age-old investing creeds of ‘Don’t Fight the Fed’ versus ‘Don’t fight the Tape’."

Global markets appear to be getting ahead of themselves. The rationale for market expectations of a quick reversal in monetary policy to easing relies on two premises: one, data interpretation, and the other historical trend projection. On data, the lower inflation print for the month of July can be interpreted as an indication of receding peak inflation. Aside from the paucity of a single data point, a close examination reveals that the weakening in the inflation print might be a symptom of some loosening of supply chain bottlenecks. While this would make the Fed’s job easier, it wouldn’t justify a near-term reversal of policy in the face of accelerated demand-driven inflation, part of it a catch-up in wages and service-related price adjustments. It can also be argued that the current stubbornly low unemployment rate could be viewed as fuel for inflation pressure, and thus calling for tightening, rather than providing respite from it. Even if inflation is assumed to have peaked, it would still take more tightening to break its hold. A long-accepted principle for containing inflation to raise rates by a larger margin than the prevailing inflation rate, and historically, it took a 20+ percent rate hike to break a peak of 15 percent inflation during the Volcker’s Fed of the early 80s.

Tadesse next hypothesizes that one of the reasons why markets have been so eager to assume a dovish pivot by the Fed is due to the central bank's "Fed Put" Pavlovian instinct. However, due to the ongoing unexpected surge in inflation, he notes that

"policymaking has gone through a dramatic regime shift recently from one of ‘promoting growth’ on concerns of deflationary pressures to one of ‘containment of inflation’ at any cost, reminiscent of the ‘inflation-containment’ policies of the Volcker era."

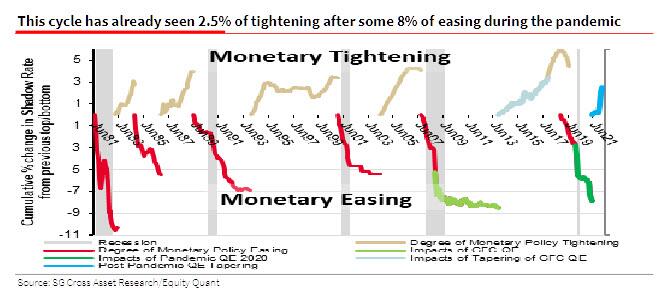

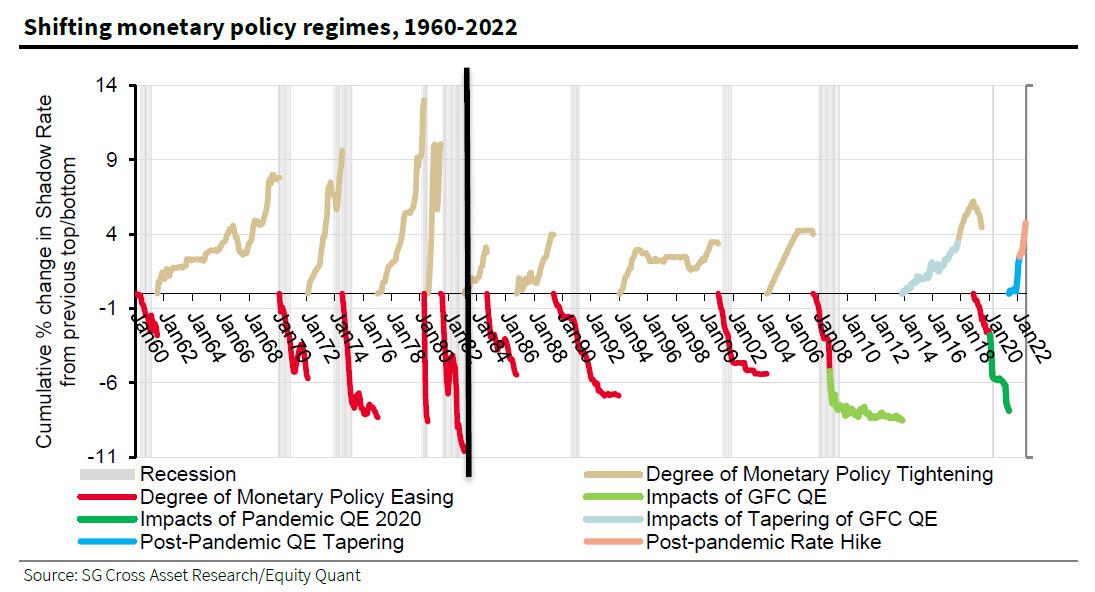

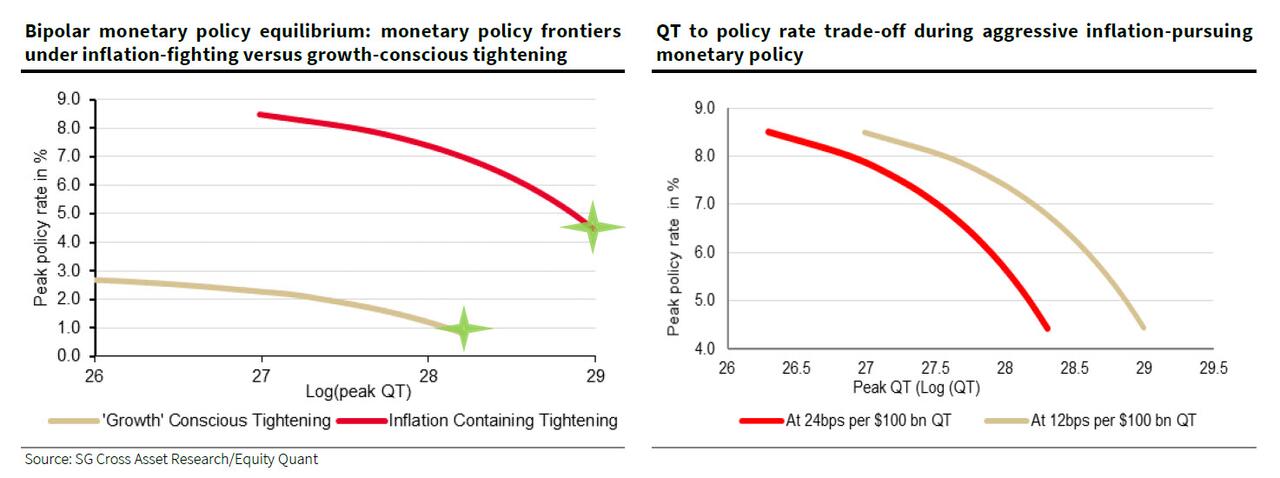

Helping to visualize this argument, the SocGen chart below shows the evolution of monetary policy over the last 60 years. As Tadesse notes, policy was driven by a need for ‘price stability’ during the inflationary periods of the 70s and early 80s when policy had a propensity to tighten rather than to ease. After the successful stamping out of inflation in the early 80s, monetary policy succumbed to fears of deflationary forces engendering chronic stagnation, which led to a propensity to ease monetary conditions rather than to tighten. But that regime seems to have changed for good now, with "unexpected" inflation raging and the Fed clearly pronouncing its monetary policy priority as containing inflation at any cost.

Thus, as we discussed extensively in recent weeks and culminating in "Even Goldman Can't Believe It: "Did Powell Mean To Be So Dovish?" if the markets' stubborn assumption to the contrary were to prove correct it could only result in an unsustainable easing of financial conditions, creating a risk of even more Fed overtightening that could rattle markets sooner or later. In fact, instead of expecting a Fed Put, the SocGen analyst writes that "one could argue that a market correction that could clear the policy channel from speculative-driven easing in financial conditions to a desirable tightening, might serve the long-term public interest." Indeed, Minneapolis Fed president Neel Kashkari made it quite clear he was personally delighted with the market dump last Friday following Powell's terse remarks. If only it wasn't Kashkari (and his Fed pals) that made the bubble that is now deflating slowly but surely possible.

Moving on: after taking a brief tangent to look at the current drivers of inflation (supply-driven is slowing, while demand-driven inflation is accelerating, and cautioning that the stubbornly low unemployment rate could be viewed as fuelling inflationary pressure than providing a respite from it), Tadesse echoes something we have said all along, namely that "monetary policy provides little help for supply-driven inflationary pressures of the type arising from supply-chain disruptions."

Indeed, it was these "disruptions" that explain Policymakers’ early dismissal of the rising inflation as transitory and something that would resolve itself in time. It is only recently that official acknowledgement has been given to persistent demand-driven price pressures. Policymakers have been clear since then that the policy stand is one of inflation-containment and has expressed this stance in deeds by allowing a meltdown of several weeks in global markets that would ordinarily have triggered a Fed Put in the past. In short, the SocGen strategist writes, "policymakers are outwardly resolved to curb inflation, even if it comes with a risk of recession" and a market crash... however, once we do get a recession and a few hundred thousand lost jobs crushing the approval rating of democrats, watch how quickly Powell will change his tune after being bombarded with daily phone calls from the Liz Karens Warrens of Congress.

So what's the Fed to do?

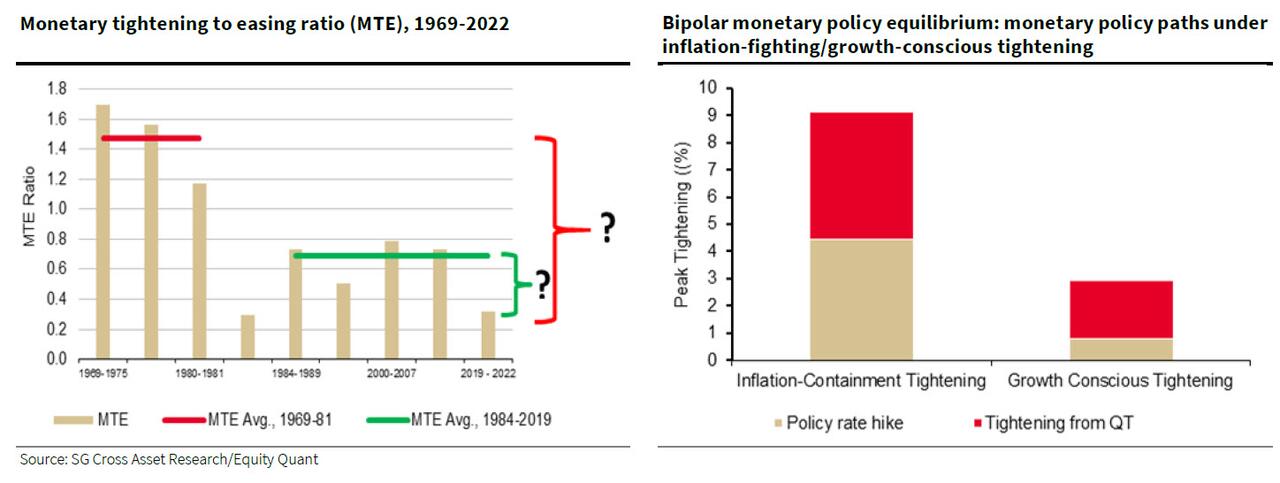

Well, in an earlier research note (which we addressed here), Tadesse argued that if monetary policy had followed a pro-growth impulse, as has been the case over the last four decades, the current tightening phase could have peaked with only 0.75-1pp of rate hikes, combined with a QT program to the tune of about $1.8tn. However, after the monetary policy regime shift to ‘inflation containment’, SocGen's analysis points to a much larger amount of rate tightening, accompanied by a meaningful slash in the Fed balance sheet. The tightening phase would take an aggressive stance, with overall monetary policy tightening going beyond 900bp and the policy rate peaking at 450bp. More importantly, Tadesse's analysis also shows that it would take implicit rate tightening of about 450bp from a QT that would slash $3.9 trillion from Fed balance sheet! The consequences for risk assets would be calamitous.

Here's how the SocGen quant gets to these numbers: as a result of the unexpected surge in inflation, Tadesse writes that monetary policy making has gone through a regime shift, with Fed’s policy single-mindedly focused on inflation containment at any cost, resembling the monetary policy framework of the Volcker era in the 1970s and early 1980s, when the average MTE ratio was about 1.5x (left-hand chart below).

The problem - as Tadesse calculates - is that such aggressive monetary tightening with a focus solely on inflation containment, even at the cost of inducing recession, would require overall monetary tightening of about 11.6%. And since rates have already been tightened by 2.5% (with only a de minimis tightening via QT for now), another 9.25% of monetary tightening might be expected via policy rate hikes and an aggressive QT program. The policy rate could go up by as much as 4.5%, with the remainder coming from QT (right-hand chart above).

In practical terms, at a rate of 12bp per $100bn of QT (SocGen had previously calculated the price impact of QT), this amounts to a QT programme of about $3.9tn, roughly equivalent to the net growth in the Fed’s balance sheet during the pandemic (which would be logically symmetric).

An important caveat in the analysis is the presumption that current inflation levels resemble those of the late 1970s through the 1980s. As recent inflation prints are the highest in 40 years, this might be a reasonable assumption, particularly in reference to the rates seen in the early 1980s. In addition, in interpreting the results, there is an implicit assumption that the current inflation prints are persistent and all demand driven. However, earlier analysis has shown that the current inflation dynamics are driven both by some transitory supply-related disruptions and demand-driven price pressures. Should the supply bottlenecks ease over time, the degree of monetary tightening needed to contain inflation through demand destruction could turn out to be lower.

To visualize the tightening "blend" achievable through both rate hikes and QT, in the above-left chart Tadesse shows monetary policy frontiers (MPF) which are all the policy rate hike and QT combinations that could generate the ‘inflation-containing overall tightening’ of upwards of 9% and the ‘growth-conscious overall tightening’ discussed earlier, with the most likely outcomes of policy combinations identified with stars. Thus, an aggressive inflation-containing policy could mean additional policy rate hikes of up to 4.5% at peak and a further implicit rate tightening of 4.5% from QT (hence $3.9 trillion in total balance sheet reduction).

In conclusion, in a time when both markets and policymakers appear too focused on the policy rate to really deal with inflation containment, and given the substantial role of Quantitative Easing policies in inducing the needed post-Covid monetary easing, the reversal policies of QT would have an equally important, albeit non-symmetric impact on tightening.

SocGen's analysis suggests that almost half of the required tightening could come from QT (about 450bp, accounting for $3.9 trillion in balance sheet shrinkage). Of course, from policy perspective, a lack of acknowledgement and clear communication of QT’s potential impacts may post the risk of overtightening. Furthermore, with markets expecting far less on the QT side, Tadesse now believes that "it could be the ramp-up in QT that could trigger the next fall in markets." Appropriately enough, it comes just as the Fed's rate of QT doubles from $47.5BN to $95BN per month.

To summarize, "it was arguably not policy rate hikes back in 2018 that laid low financial conditions, leading to a surprise pivot in monetary policy in December. It was rather gently accelerating QT in the background. In the same token, it could be a ramp-up in QT, this time on a larger scale to erode a much larger balance sheet, that may surprise markets."

One final point: is there a snowball's chance in hell that the Fed will do almost $4 trillion in QT? Of course not: as we explained on July 14, when we quoted from former NY Fed and current BofA iconic Fed analyst, Marc Cabana, the Fed will be forced to end QT prematurely (in no small part because BofA's base case forecast is now for a US recession in 2023), and as such, "Fed QT that is stopped in Sept ’23 will result in $1tn less balance sheet reduction vs our prior estimates through end ’24. Over a similar period, early QT end would result in $780b less UST financing need + $350b of additional Fed UST demand."

Cabana, is of course, correct: there is no way that the Fed will be able to do years of QT at a pace of ~$100BN per month to hit SocGen's bogey without pushing the US into a full-blown depression (especially since the recession has already officially started). But it will take a few months of -300,000 payroll prints for markets to pivot again, and realize that when Powell vowed the Fed would not even think about think about pivoting in 2023, he was wrong... again... as usual.

The implication, however, is even more profound: if Tadesse is correct, and if indeed the Fed is unable to contain inflation unless it tightens by 9% in some combination of rates and QT, that means that the Fed will begin its next easing cycle with inflation well above the Fed's target. Which incidentally, is how this game ends: with the Fed hiking its inflation target from 2% to 3% (or more).

Impossible, you say? Not at all: Europe is already setting the stage for what is not only not impossibly but inevitable.

And yes, once the "inflation target" trial balloons start floating, readers better have all their net worth in the form of risky assets, gold, crypto and so on, because in the span of nano seconds, the entire asset market will reprice exponentially higher as the Fed finally admits it has to throw in the towel.

Aucun commentaire:

Enregistrer un commentaire