(C'est bien, l'un de ceux qui attaque la livre turc prévient. note de rené)

Game Over For Turkey As Net Reserves Turn Negative, Morgan Stanley Sees Lira Collapsing

One week ago, when the Turkish Lira first tumbled below 20 against the USD, we warned that much more pain was in stock based on a rather dire analysis by Goldman of the central bank's reserve position, a much more ominous factor for the coming currency collapse then Erdogan's reelection.

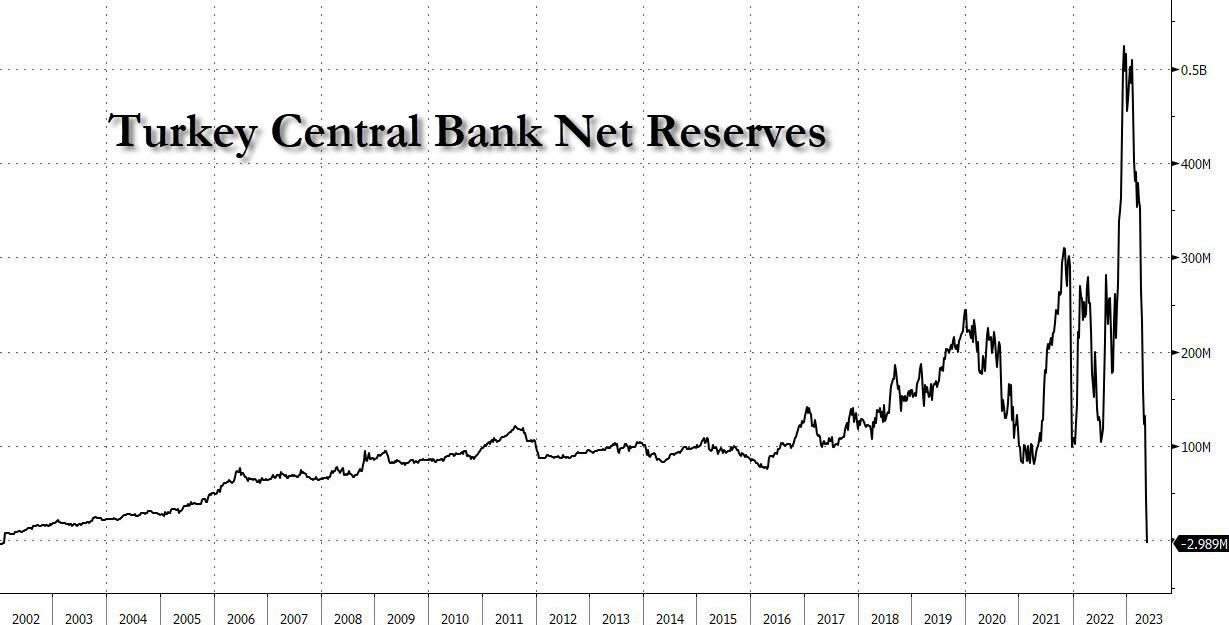

Since then it's gone from bad to worse, with Reuters also jumping on the bearish lira bandwagon and reporting that the Turkish central bank's net forex reserves dropped into negative territory for the first time since 2002, standing at $-151.3 million on May 19, as the bank - following Erdogan's strict orders - scrambled to counter demand for hard currencies (USD, gold, crypto) ahead of Sunday's runoff vote.

Forex demand in Turkey surged to record levels ahead of May 14 on companies' and individuals' expectations that the lira, which lost 44% in 2021 and 30% in 2022, will plunge after the vote (spoiler alert: those fears have been justified).

As we discussed last week, the central bank's forex reserves have sagged in recent years due to costly market interventions and other efforts to cool forex demand. The bank's net reserves dropped by $2.48 billion in the week to May 19, to their lowest level since February 2002. They have dropped $27.7 billion since the end of 2022, and were at negative $3 billion as of May 19. The net forex reserves would be even more negative if outstanding swaps, courtesy of foreign central banks and which stood at $33.50 billion on Wednesday, are deducted (as they should be since the CBRT will have to repay these at some point).

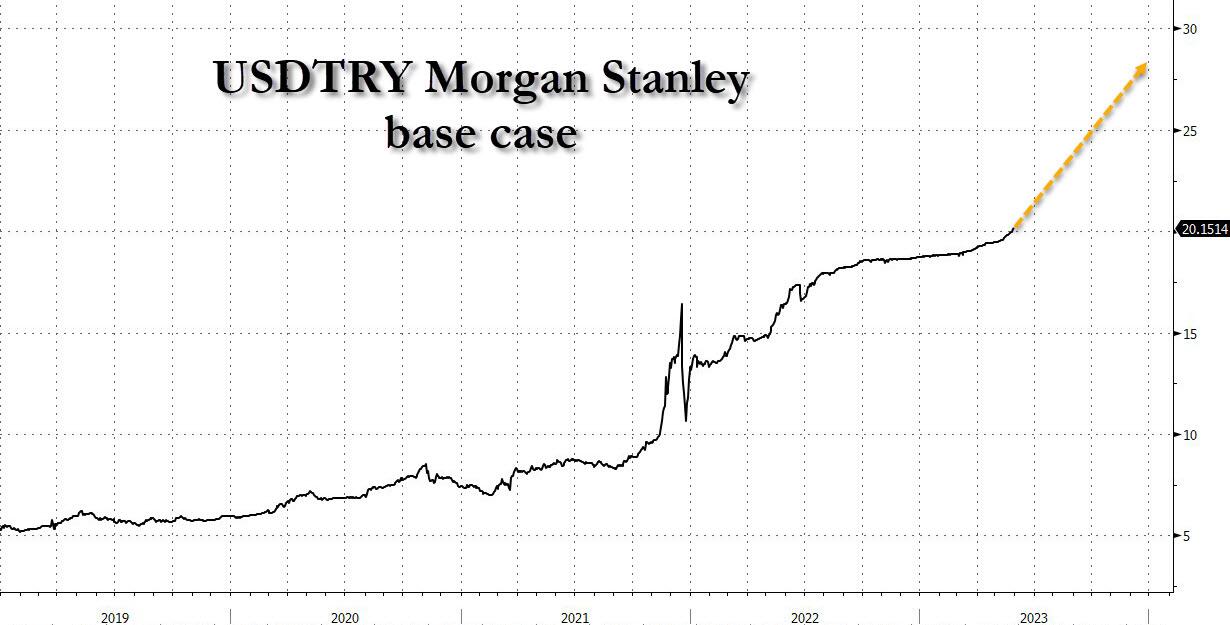

And while the endgame here is clear to all, few are willing to say it out loud for fear of retaliation by the Erdogan regime (no really, he has been known to throw people in jail for recommending a Turkish lira short); yet one bank which decided to double down on Goldman's dire view of how it all plays out is Morgan Stanley, which in a note last week (available to pro subscribers in the usual place), wrote that the turkish lira plummeting to 28 by the end of the year, is likely in the cards (in our view, that's a rather optimistic take since the lira is about to become the new Bolivar where soon new zeroes are added daily if not hourly).

According to Morgan Stanley strategist Hande Kucic, in the absence of conventional monetary tightening - which clearly will not happen in a world of Erdoganomics where lower rates are somehow expected to lead to lower inflation and where Erdogan will not allow higher rates even if it means crushing hyperinflation - post-election macro adjustment, i.e., external rebalancing, would have to rely more on exchange rate depreciation and a tightening in financial conditions through other instruments and regulations. As such, Morgan Stanley thinks that the policy authorities will adjust alternative instruments, including the CBT’s liraisation and reserve-management strategies, to:

- Let the currency depreciate at a faster pace;

- Let deposit and loan rates go higher;

- Restrict loan supply; and

- Tighten regulatory controls over locals’ FX transactions.

Looking at the chart above, Kucic notes that "the deterioration in the CBT's net FX reserves position in recent weeks suggests that a more front-loaded adjustment in the currency may be necessary versus our previous expectation for the path in the scenario of victory for President Erdogan" (if not ours: Zerohedge has been telling our premium subscribers that a short TRY position is our highest conviction trade for a long time). And, sure enough, the market has reached the same conclusion, with a more front-loaded adjustment priced in already.

Morgan Stanley's conclusion is that while the bank's pre-election scenario note stated that USD/TRY could reach 26 by the end of the year and in a back-loaded fashion "the risk is that this level is reached sooner, with a higher USD/TRY level by the end of the year, closer to 28, absent a change in policy direction, particularly on interest rates."

Spoiler alert: there will be no change in policy direction, as Erdogan is going all the way down with his ship.

And so, "without a change in the macro policy framework to prioritize disinflation and to adopt market-friendly policies, Turkey's high external finance needs will likely keep macro risks alive, increasing sensitivity to global shocks (commodity prices, Fed) as well as the availability of FX inflows from regional partners."

Here is a visual recap of what Morgan Stanley thinks will happen next:

Alas, with hyperinflation rampant, and with Erdogan no longer having FX reserves to sell, besides gold which he will most likely seek to pillage for himself as he slowly but surely prepares to depart for a non-extradition country, we are confident that the USDTRY hitting 28 will take place not in December, but in a few weeks.

More in the full Morgan Stanley report available to pro subs.

Aucun commentaire:

Enregistrer un commentaire